Drawing On Allowance

2024 is the year of making money!

Or giving it away.

So far, there has been a massive amount more outgoing than incoming, but I hope that next month I will be able to get back on track and break even. However, I am also looking to be more active teaching my daughter, Smallsteps, about money, money flow, value, saving, spending, needs, wants, delayed gratification... The list goes on.

And today, was the first day of her new life.

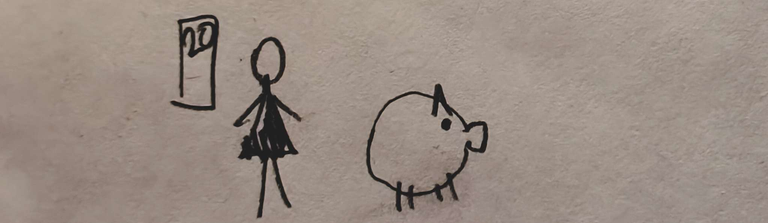

Payday.

This wrinkled 20 was the first allowance payment she has received. 20 sounds like a lot, but it is twenty a month, which my wife thinks is still too much. In my opinion, it is a bit like the army here, where the "pay" is enough to cover a packet of cigarettes a day. However, since my daughter isn't much of a smoker, I decided it should be enough to cover a bag of candy, and a soda.

She barely eats candy. Never had soda.

My thinking is that she should be able to cover something with it, if she needs. But, I also wanted to make it monthly for other reasons.

1) Larger amount

Having it as a larger amount means that it is harder to spend, because it seems more significant. Getting money in dribs and drabs (weekly) means that you can constantly spend, but can't get very much. Having the amount be more significant, means that she can also get something more significant.

2) Having to wait

Patience is a virtue, especially when it comes to personal finance and investing. The general level of patience these days seems incredibly low, which combines with a very short attention span to utterly destroy the chances of building an investment mindset. Smallsteps is going to have to do her various tasks and net get "rewarded" for them for up to four weeks. She has to invest her current actions, for a future gain.

3) Greater impact

Getting more all at once, also means that she sees that bump in her piggybank. She got the piggybank for Christmas (a large, fluffy pig), and she is only now starting to use it. We counted up all the money she had, including all the shrapnel (coins), so she knows how much is in there. This took us a little while, as it was a teaching moment for counting, grouping, and having some fun. Now, when she gets some money for her allowance next month, it is going to make an impact on the total. It is going up be tens, not by singles.

Now, Smallsteps doesn't really need money, and we don't expect her to pay for much, but having some money that comes on a schedule, means that she has some stability. The monthly schedule is used (my wife wanted weekly at first), because I get paid monthly. My theory is that the people who get paid weekly, probably struggle with money more than those who get paid every fortnight or monthly, as they don't have to manage their money as closely, because they are never "that far" away from a payday. I want Smallsteps to recognize that a month can be a long time, even though she is a little too young to learn the lesson yet, but we are going slow.

But as she doesn't need money most of the time, we are going to have to engineer some opportunities for her to spend some, as well as opportunities to not have enough to cover what she wanted. We have done this already, starting last summer at the zoo, where she wanted to buy two, small, soft toys from the giftshop, but only had enough money for one.

I made her decide.

In the end, she made the tough decision, but asked to have a photo with the one she was leaving behind, so she wouldn't forget it. She wasn't upset at having to make the choice, she was sad for the one that would miss out on coming home with us. Five minutes later, a typical then six year old, was happily playing with her new toy.

And today, I drew a diagram and told a story of how money flows, even when there "is no money", because she was interested to know. The other day I told how I got on the bus for free, because the card machine was broken and I didn't have cash. Smallsteps then asked if using the card means that the money isn't lost.

So, the diagram was of my work, a few banks, a shop, a bus, an ATM, and Smallsteps. I showed how I work for money, but don't get paid in cash. Instead, I have a bank account, as does my work, and then we played a game of working, getting paid, shopping, going on a bus ride, getting cash out of an ATM and crediting and debiting along the way. Smallsteps was doing the math of 10 from here to there, 2 from there to here, and so on. Eventually, I took twenty out of the ATM and gave it to her, where she deposited it in her drawing of her piggy bank.

While all this is very basic, going through the processes, drawing the pictures, talking it through, having her do the math, joking about different things and, setting up scenarios like "buying too many puppies (her story) and not having enough money to pay for food", help her to get an understanding of the flows and hopefully, take away a lot of the stigma that is set up around money in society. At least, I want her to be able to speak openly to me about it.

After she went to bed, my wife and I paid the bills that have been mounting up as we have been forced to front a lot of additional expenses. Looking at my bank account a day after payday and thinking, a month is a long time, is a reminder that I need to be better with my finances also.

Perhaps I should draw more diagrams.

Taraz

[ Gen1: Hive ]

We learn by teaching others, right?

This is my explanation of "those that can't do, teach" - It isn't about not necessarily being able to, but teaching something requires looking from different perspectives. It is useful for me to have to simplify it all down for her.

Spending money, in theory, should be a source of satisfaction. Basically because if you spend it, it's because you have money to spend, right?

This story is not as simple as it seems. There are, for example, people who spend compulsively and have a hard time when they can't pay the bills. Or those who have had a life of deprivation and when they have the chance to spend, they restrict themselves on even the most basic things for fear -consciously or unconsciously- of falling into poverty again.

Others are devoured by their own greed and prefer to take their money to the grave. The list of reasons associated with the fear of spending money is very long. But when this behaviour starts to interfere with the normal course of life, it is likely to be a rare condition called chrometophobia (chrometophobia is the extreme fear of spending money).

We often emphasise the importance of financial education, such as gaining a solid understanding of how money works and having the resources to make informed decisions.

But when it comes to establishing financial health, one thing most people don't consider is their financial personality type, or their approach and emotional responses to money.

We each have our own beliefs and emotions about money, and they are mostly shaped by our individual life experiences.

Are you a “compulsive spender” type?

Even if they have large amounts of debt, compulsive spenders will often continue to shop. They may even try to hide large purchases from friends and family. In extreme cases, they may risk bankruptcy if they consistently spend more than they earn.

Yes. I have a scarcity mindset, largely built from my experiences for the first 35 years of my life. The last ten, I have been shifting this. An abundance mindset doesn't mean spending like water and hoping more arrives through :)

The economy encourages compulsive consumption through every business model. No company looks to improve the financial health of society, because every company wants to make profits.

One of the problems I see every day is people who can't manage money. I don't mean to denigrate people who are truly struggling, but there are plenty of folks who have incomes I would consider truly affluent who still live paycheck to paycheck. Deferred gratification, saving, investment, living below one's means, budgeting to take control of expenses, recognizing opportunity costs, all of this is apparently unknown to most.

I lived in a single-income blue-collar middle class household. I helped my mother clip coupons, plan expenses, and make the most out of what we had while still saving and tithing as a part of home-schooling. I don't think many Gen X, Millennials, or Zoomers have had that kind of experience. The consequences are everywhere. Avoidable consumer debt looms as a constant threat for so many people. Instant gratification and deferred payment is the inverse of healthy financial planning.

So good job teaching Smallsteps early on to start considering these subjects!

It is amazing, isn't it? I know at times I am far worse with money than I should be, but at other times I am far better with it than most, which saves me. I also tend to work my ass off at what I do, which brings some benefits.

I don't think so. Though, I am Gen-X and most of my friends were working from around 16 years of age on. For me, I was working from 12 with cash in hand jobs, as it was the only way I could get money for anything I wanted. It taught me independence, but not sure if for better or worse yet.

A friend of mine (from the US) brought up how many people are living one paycheck away from nothing. It is incredible that society functions at all there - but then, that is what the gaps are there for - so that the affluent part, don't see much of the financially effluent part.

A lot of the wealth of the "1%" is in fact highly leveraged debt, or shares in highly leveraged corporations. It's a house of cards waiting for the inevitable economic reality behind the facade of prosperity to be revealed. We'll see what stands after. But of course the US government will plunder the productive economy to prop up their cronies when they get caught with their pants down. That's the reality behind the rhetoric of our "free-market capitalism."

Such a great lesson, and encompassing a good half or more of all the math American children learn in seven years of schooling. And applied math at that, something none of our kids learn how to do anymore. Well done!

I'm surprised you have to lay out all the money like this. In the US, the insurance companies pay, all I've ever had to do is to sign forms. What happens to someone who has insurance, but no hedge fund to lend money to the insurance company, which is what this amounts to?

I find this so silly. Teaching things that kids aren't able to connect to their daily lives in any way. Keep the grades up, but not know what is learned.

Are you white? :D

I really do think it has to do with the last name. All I have ever had is problems, no matter how long I have had the insurance, how much i pay - my friends however have had almost zero issues.

Good question!

If I added up all the money I have spent on insurance "premiums," and had saved all that money instead of paying those protection fees to that mob, I would have come out way ahead financially. This is why insurance companies make money. I'm so sorry you have to deal with this, it sounds awful. But good job helping small steps through it, she will understand ups and downs.

Big day for her!

I wonder if she is completely aware of the world she is entering into.?

Reading your post made me think how I would approach that now there is crypto around. Maybe it would be a nice challenge to encourage a kid to learn to earn and be their offramp when he/she wants to cash out, putting a monthly limit.

It sounds like to have some very helpful lessons in store for her! My allowance was two dollary per week if I remember right.

Congratulations @tarazkp! You have completed the following achievement on the Hive blockchain And have been rewarded with New badge(s)

You can view your badges on your board and compare yourself to others in the Ranking

If you no longer want to receive notifications, reply to this comment with the word

STOPWhen my children were young, I was giving them an allowance of CAD$50 per month, but they had to buy their own clothes and shoes. I thought that would teach them how to deal responsibly with money. And, at the same time, I did not need to count how much I had spent for each of them.

I like this. First lesson on the personal finance. I suppose lesson like this would set the tone for the further progress of the financial decisions in the near future. And it's good to see that paying for food is something thought with plan in mind. Which shows deeper understanding of organization. Indeed 24 is the year of Saturn as they say discipline, finance and plan.

She really sounds very advanced for her age. Is it too early to teach her about taxes? Haha

But I really like what you are doing here. Teaching her about these concepts at a very young age is nice. I remember getting allowance in elementary, and it was a weekly thing. I don't remember buying much from it, and I just saved it most of the time.

Patience is a virtue, especially when it comes to personal finance and investing,

This is so incredible I think this is the right thing to do nurturing her to understand the effect of money and how it works in the society and in our lives is the best gift any parent can give to their children, I know small step will definitely grow to be very prudent n wise like her Daddy 😇

Yesterday I did more math than normally... I tried calculating if it is worth selling my level 3 HYDRA. I decided that it should be worth it. So I am trying to sell for 250. Now we will see if I will have enough patience to sell it.

I think this is good. This will teach her three things.

Firstly, she will be patient just like you have said. She will be able to wait till the time she knows that her monthly allowance will come in. It will help her when she grows up because she may eventually get a job that pays monthly so she will be used to it and know how to spend her money that one won’t finish before she gets the other.

Secondly, if she gets it everyday, she will want to buy things that are not really relevant with it but if it is monthly, it is possible for her to at least list all of the things she wants and buy them if they are relevant.

Lastly, she will be able to save. Getting money everyday or weekly may not allow some people to be able to save. They believe another money will come soon so it is always better monthly and you will be able to save especially when you are dedicated to

Soo work make money and chill no matters what

What an article. It reminded me the time when I was a kid and had a small "paycheck" as well. It was not that much and my parents sometimes made me offering dinners with my money. Lol.

Still, I never used them to buy candies or foods but I preferred using them to buy things to read or to play with. I perceived they had "higher added value" than "consumables" :D

My son earns 5 HIVE a day for good grades in school. And he now has a passive income of about 150 HIVE per month from a capital of 5000 HIVE. He likes this game, maybe this is one of the reasons why he has the highest score in all subjects :)

Hello tarazkp!

It's nice to let you know that your article will take 8th place.

Your post is among 15 Best articles voted 7 days ago by the @hive-lu | King Lucoin Curator by blind-spot

You receive 🎖 0.8 unique LUBEST tokens as a reward. You can support Lu world and your curator, then he and you will receive 10x more of the winning token. There is a buyout offer waiting for him on the stock exchange. All you need to do is reblog Daily Report 186 with your winnings.

Buy Lu on the Hive-Engine exchange | World of Lu created by szejq

STOPor to resume write a wordSTART